Last week a group of technologists, including Bruce Schneier, sent a letter to Congress outlining their concerns around cryptocurrency and urging Congress to regulate the space.

Now let me be the first to say that I broadly support this goal. I have no problem with the idea of legislators (intelligently) passing laws to regulate cryptocurrency. Indeed, given the level of insanity and the number of outright scams that are happening in this area, it’s pretty obvious that our current regulatory framework is not up to the task. If the recent letter simply asked for intelligent regulation, I’d gladly sign onto it. Unfortunately that’s not at all what this letter says. Instead, it argues that the entire technology field is worthless and cannot be used for any practical purpose.

Don’t take my word for it. I urge you to stop reading this post right now and take a look for yourself. I’ve helpfully reproduced some of the critical pieces below (emphasis added):

By its very design, blockchain technology, specifically so-called “public blockchains”, are poorly suited for just about every purpose currently touted as a present or potential source of public benefit. From its inception, this technology has been a solution in search of a problem and has now latched onto concepts such as financial inclusion and data transparency to justify its existence, despite far better solutions already in use. After more than thirteen years of development, it has severe limitations and design flaws that preclude almost all applications that deal with public customer data and regulated financial transactions and are not an improvement on existing non-blockchain solutions.

…

The catastrophes and externalities related to blockchain technologies and crypto-asset investments are neither isolated nor are they growing pains of a nascent technology. They are the inevitable outcomes of a technology that is not built for purpose and will remain forever unsuitable as a foundation for large-scale economic activity.

Frankly, this whole letter bums me out. Over the years I’ve spent a decent amount of time on Twitter calling out cryptocurrency shills who spout technical nonsense while promoting outright confidence games. I took for granted that my technical colleagues would be more a little more reasonable, particularly when speaking as technical experts to Congress and regulators. This is not simply someone “being wrong on the Internet.” These are important claims that deserve serious attention, and there are real consequences to being wrong here.

So while I appreciate the authors’ intentions, against my better judgement — and you’d better believe my better judgement is shouting at me for writing these words — I feel compelled to say something in defense of this technology area. “Public blockchain” technology enables many stupid things: today’s cryptocurrency schemes can be venal, corrupt, overpromised. But the core technology is absolutely not useless. In fact, I think there are some pretty exciting things happening in the field, even if most of them are further away from reality than their boosters would admit. Moreover, many of crypto’s technical problems are also amenable to some really exciting technical solutions, many of which are already here or on their way to deployment.

So instead of enjoying a beautiful week of Baltimore summer, I’m going to spend my time indoors, writing about what I think those things are — and (more or less incidentally) why I think these distinguished authors are wrong that “public blockchain technology” is a technical dead end. This post is not precisely a rebuttal to the letter above: instead, I’ve decided to phrase it as a general response to some of the more common spurious objections I hear people make to public blockchain systems. It just happens to be the case that a few of these (but not all) come up in the letter.

Finally, in the interest of full disclosure: I have designed privacy-preserving cryptocurrency systems (and still serve on a Foundation board of one), and I’m currently working on a startup that is trying to add regulatory compliance capabilities to public blockchains. (You can decide for yourself if this makes me a shill for Big Blockchain or Big Regulation. Frankly I’m not sure.)

Objection: “Cryptocurrency is terrible for the environment”

It’s probably best not to beat around the bush on this one: the most serious current objection to cryptocurrency (as it’s currently construed) is the massive environmental impact of proof-of-work (PoW) mining. I won’t devote a single second towards minimizing this concern. Many defenders have tried to paint the electricity consumption of Bitcoin and other PoW currencies as “green” or define it as a form of energy storage. This is dishonest nonsense: estimates hold that at east 60% of mining energy consumption still comes from fossil sources.

And that’s a lot of energy.

The totals depend on which smallish nation we’re using as our standard unit of energy consumption: this September 2021 NYT article has Bitcoin (all by itself) consuming nearly as much energy as Finland. Yet whereas Finland produces Nokia cellphones and lovable wooden clogs, Bitcoin just produces… bitcoin. Not to mention a pathetic transaction rate of about 3.5 tx/second across the entire globe, as of this week.

Regardless of where you stand on cryptocurrency as a technology, you should understand that this wasteful resource consumption colors the public’s views of cryptocurrency in a highly negative way, and it is absolutely right for people to have these feelings because we are in a climate crisis and wasting this much goddamn energy on a single consensus protocol is pointless, harmful, and quite possibly evil — particularly when the result of all this energy consumption isn’t even a particularly decentralized network.

However: before you call for some kind of misguided cryptocurrency ban, you should understand that this is a temporary situation and not an intrinsic component of public blockchain technology.

Proof-of-work was chosen early in Bitcoin’s history because Bitcoin was designed to be operated by volunteers with personal computers. The concern in this setting was that a single user could mount a “Sybil attack” and pretend to be many different computers, thus dominating the construction of blocks on the network. Since verifiable real-world identities didn’t exist on the Internet, Nakamoto chose proof-of-work as an elegant solution: this approach makes your “vote” in the network organization proportional to the amount of computing power you possess. Since the typical early Bitcoin user only had one or a small number of computer CPUs to mine with, this kept the early Bitcoin network relatively decentralized.

Unfortunately modern proof-of-work mining looks nothing at all like the early Bitcoin network: today’s mining is a capital-intensive industry that competes to build entire datacenters full of specialized ASIC-based mining hardware. This change has undone most of the early decentralization benefits, while pointlessly burning tons of coal and natural gas.

But all is not lost.

Proof-of-work is not the only technology we have on which to build consensus protocols. Today, many forward-looking networks are deploying proof-of-stake (PoS) for their consensus. In these systems, your “voting power” in the network is determined by your ownership stake in some valuable on-chain asset, such as a new or existing electronic token. Since cryptocurrency has coincidentally spent a lot of time distributing tokens, this means that new protocols can essentially “cut out the middleman” and simply use coin ownership directly as a proxy for voting power, rather than requiring operators to sell their coins to buy electricity and mining hardware. Proof-of-stake systems are not perfect: they still lead to some centralization of power, since in this paradigm the rich tend to get richer. However it’s hard to claim that the result will be worse than the semi-centralized mess that proof-of-work mining has turned into.

And proof-of-stake is no longer theory. It’s already been deployed in production within a number of successful projects, including Avalanche, Cardano, Algorand, and Tezos. The Ethereum project is in the process of rolling out a proof-of-stake upgrade they call “Ethereum 2”, and while the final plans still seem a little handwavy for this late date, there has at least been some real progress in launching parts of the system. Beyond proof-of-stake, there are other technologies in deployment, such as the proof-of-time-and-space construction used by Chia, or more centralized proof-of-authority systems.

Now, admittedly: none of this solves the problem that much cryptocurrency is dirty today.

But the question we should be asking is not whether to be angry about the power consumption of proof-of-work mining. We should be trying to figure out the right path out of this mess. And more concretely, whether there’s a path forward which is more likely to produce a good outcome than what is already happening in the industry — namely, that projects are rapidly deploying cleaner technologies to replace proof-of-work. Because it’s very unlikely that shade or hypothetical cryptocurrency bans are going to fix the problem any faster, and in fact: government overreaction could make it much, much worse by driving resources away from the cleaner chains that are coming online to solve the problem.

Objection: “Public blockchains can never support banking features like transaction reversal.”

One of the biggest problems in the field of cryptocurrency is that too many technical experts stopped looking at the field around 2015. This means they’ve missed a lot of the more interesting developments that have occurred in the past couple of years.

To give an example of this phenomenon, let’s take one claim that occurs very near the top of my colleagues’ letter:

This claim is not technically accurate. And worse, it indicates that the readers have missed several years’ of business and technological development. Unfortunately, correcting mistakes like this requires diving pretty deep into the technical weeds.

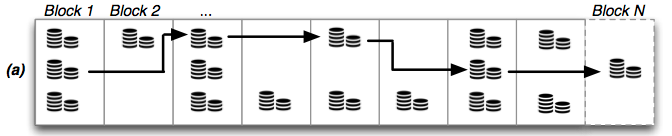

Blockchains work by assembling a data structure called an append-only ledger. Much like a traditional pen-and-paper bank ledger (shown at right), this ledger represents a list of events, such as currency transactions. A common feature of blockchain tech is that the ledger is constructed using a kind of “adversarial collaboration” that runs between many different computers. The upshot of this process is that entries on the ledger are very difficult to tamper with.

In the earliest cryptocurrency systems (like Bitcoin), the ledger is used to record the ownership and transfer of made-up tokens, such as the bitcoin currency. Since there is no trusted party or “bank” that manages the accounts on these systems, Bitcoin’s transaction rules are very simple and work like cash. If I sent money to your account, only you (using a cryptographic private key) should be able to control where it goes next. This is exciting and also a bit scary: there is no “undo” feature in these cash-like tokens.

By contrast, the modern retail-facing credit card and banking industries work very differently. In those industries there exist trusted parties (your bank or credit card’s customer-service representative) who can and do “reverse” fraudulent or mistaken transactions under specific circumstances. (Whether they will do so is a very different question.)

While it’s technically accurate that blockchain ledgers cannot easily be overwritten, it’s critical to understand that ledgers really has nothing really to do with transaction reversibility — any more than the specific writing instrument used by a historical bank (pen vs. pencil) determines whether a bank can reverse transactions. In practice, transaction reversal has nothing to do with the way a ledger is written. Transaction reversal is not about ledger technology, it’s about transaction rules and trust: it requires that there is someone that you trust to make transaction in your accounts without your explicit permission.

In other words, transaction reversibility is not about the ledger, but rather about the transaction rules that a currency uses. A reversible currency requires that someone anoint this trusted party (or trusted parties) and that they use their powers to freeze/burn/transact currency in ways that are at odds with the recorded owners’ intentions. And indeed, this is a capability that many tokens now possess, thanks to the development of sophisticated smart contract systems like Ethereum, that allow parties to design currencies with basically any set of transaction rules they want.

And what’s fascinating is that none of this is hypothetical!

One of the most interesting developments of the past several years is the deployment of several government-regulated “stablecoins” that represent tokenized versions of real fiat currency (e.g., dollars) in a bank account. More or less without exception, these regulated currencies, which are issued by licensed and government-regulated organixations like USDC and BUSD (and are not the same as unregulated algorithmic scam coins like UST) each possess a centralized party/committee that can “freeze”, mint, or “burn” money owned by any user in the system [BUSD code, USDC code]. A centralized manager of the currency can therefore “lock” the account of any illegitimate recipient and compensate the spender directly, or in some cases, the centralized manager can “burn” and mint new currency to send back to the originator.

Indeed, this capability is explicitly mandated by regulators:

It is reasonable to point out that, compared to mature banking systems, current stablecoins’ transaction reversal capabilities are quite rudimentary. From a business perspective there is no guarantee that a coin issuer will return your stolen money, nor that they can do so in the event that a thief has already passed your money on to a fence. (Just as there’s no guarantee that Zelle will do so.) Modern banks implement these features with fraud-detection features and with a combination of delayed settlement, insurance, and trust. Some of these are technical capabilities, but many are largely business questions. In either case, none are “antithetical to the design of public blockchains.” If reversibility is actually important to you as a feature, then you should pay attention to how these new regulated systems develop.

(issued by Circle/Centre). Chart shows market capitalization from near-$0 in 2020 to about $60bn today.

Objection: “Cryptocurrency doesn’t scale [or the fees are too damned high]”

The early Bitcoin protocol was designed to be many things, but fast and efficient was not one. The system’s famously low transaction rate is effectively the result of several tradeoffs in the design of the network’s consensus algorithm: where centralized payment systems like Visa or Mastercard can scale horizontally — by assigning different computers to handle various subsets of user transactions — in Bitcoin (and Ethereum, and most other extant platforms) every single participating node must validate every single transaction made by anyone in the system. This means that simply adding more computing power doesn’t produce a faster network.

The result is pretty dismal. Bitcoin’s transaction rate has historically topped out around 7 tx/sec worldwide (although recent upgrades may improve things slightly.) Ethereum pulls off maybe 20-30 tx/sec by sailing a bit closer to the wind. Meanwhile: networks like Visa handle about 1700 tx/sec on an ordinary day (!), and 10x that rate on major holidays.

This scaling problem makes cryptocurrency unworkable for just about any mainstream payments application. A single popular mobile game like Candy Crush probably conducts enough in-game transactions to challenge the Ethereum network.

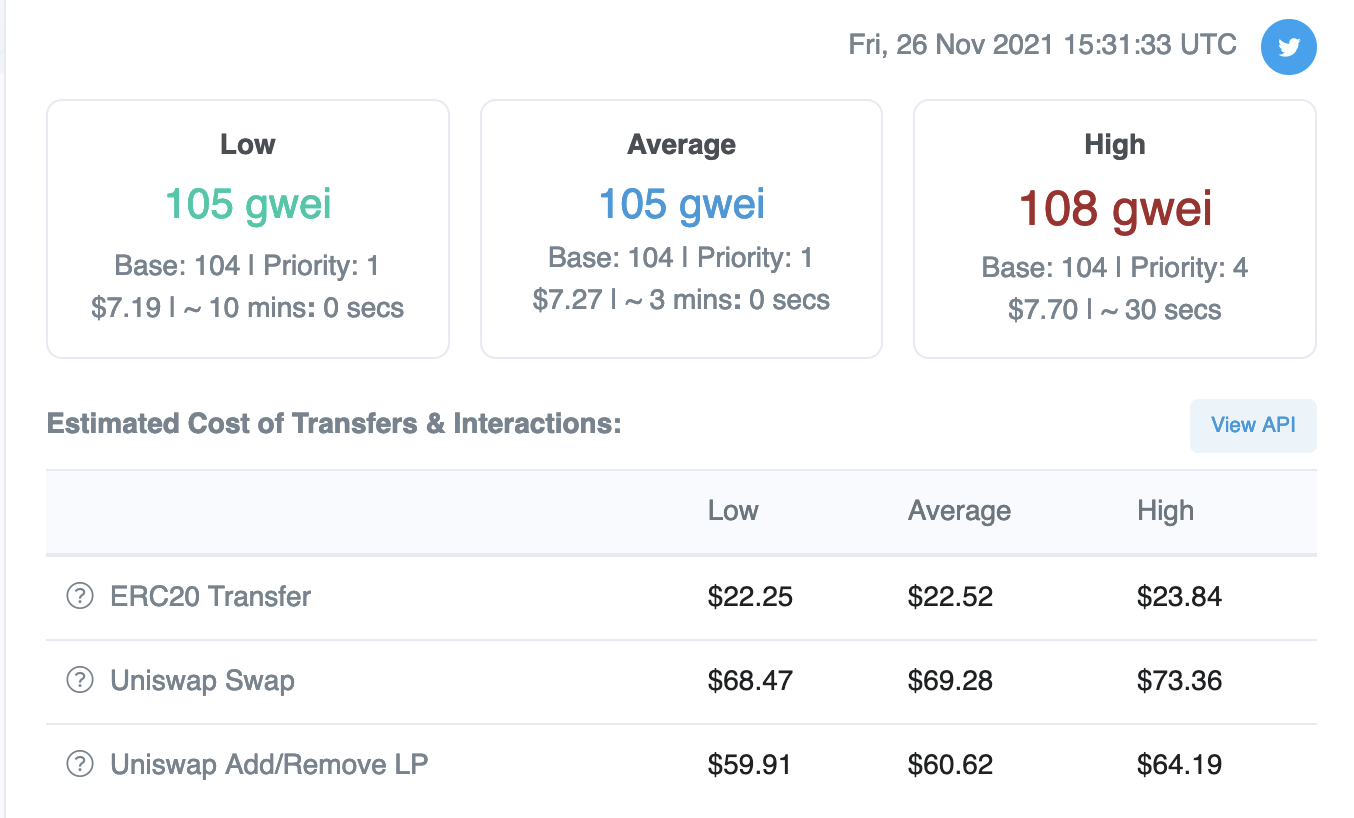

And because the transaction rate in these so-called Layer 1 (L1) cryptocurrency networks is so low, competition for scarce network resources translates into high transaction fees. That’s why it recently cost $22 (!) to send a single token transaction on Ethereum, and much more to handle sophisticated transactions like DeFi swaps. These prices are fine if you’re a crypto speculator doing $1,000+ trades. But they rule out anything as mundane as paying people.

This sounds pretty bad. However, an important lesson I’ve learned in my career is this: if people are sufficiently motivated and the only barrier is an engineering problem, then it’s probably wise not to bet against them.

With some exceptions, the cryptocurrency community has acknowledged that existing techniques are unscalable, and they are engineering to try to get around this. The result has gone in two different directions. Both are unproven, and the resolution of these developments will determine exactly how well the field can grow in the future.

More money, more networks. The most obvious way to scale L1 cryptocurrencies is just to build more of them. This describes a lot of the action in 2019-2021: as networks like Ethereum saturate with transactions and become expensive, new entrants are deploying compatible (and sometimes incompatible) chains that provide more transaction capacity without the fees. These networks often look like Ethereum (in that they’re Nakamoto-consensus, proof-of-work mined systems), but sometimes they’re stripped down or use faster consensus technologies (examples include Avalanche, Polygon, Celo and Solana.) Some are just centralized clones of Ethereum.

This might stave off total chaos, but it probably isn’t sustainable. Even if all these networks work perfectly — and that’s a big assumption — the problem with adding more networks is that your ecosystem fragments. If funds are on the Ethereum chain and you want to use an application that lives on a different network, how do you get your funds over there? The solution today mainly involves “bridges” — semi-centralized parties that will accept your money on one L1 network and provide you with funds on another. If you want to move your funds back to the original network, that’s another pass through the bridge, with fees on both networks. It also means you have to trust the integrity of both the bridge itself and the destination network, which might itself be much less robust (and safe) than the original network you started from. It’s possible this approach will work well enough to enable most applications, but I wouldn’t bet on it.

Rollups. The second approach, heavily promoted by the Ethereum Foundation, is to improve the scaling of individual L1 networks like Ethereum by performing transactions on some second-layer, with the most common proposal being a “rollup server.”

Rollup servers are centralized machines that can validate many transactions quickly. One rollup server doesn’t handle every payment or smart contract on the chain. Instead, it operates over one or a small number of applications (say, a few specific smart contracts.) Users submit their transactions either to the chain itself, or directly to the server, which then validates the transactions and posts a short “proof” to the L1 chain asserting that a large collection of transactions has been checked and found to be valid. The idea here is to reduce the amount of computation and storage that the L1 nodes must perform to check these transactions: rather than validating 10,000 individual transactions, the L1 nodes simply verify one short assertion posted by the rollup server.

This sounds like magic, and it is, sort of. There are two approaches to building rollups, both of which are in “experimental” production today:

- Optimistic rollups use a “trust and punish” approach. The rollup server posts a financial bond to assure the world that it will correctly validate all of its transactions. In the unlikely event that the rollup server “cheats” and authorizes an invalid transaction, any third party whistleblower can submit a “fraud proof” that proves the rollup server’s failure. The L1 network can check these proofs, which will invalidates the bad transactions and pay the whistleblower a large reward.

- ZK rollups use cryptographic technology drawn from the field of zero-knowledge protocols, such as SNARK or STARK proofs, so the server can “prove” that all transactions were validated correctly before it posts the summary results to the chain. In principle this means the L1 chain can verify a short “proof” that covers many thousand complicated transactions, with (essentially) no possibility of cheating.

Rollups sound like a terrific idea, and the Ethereum community has bet heavily on the tech. But it’s worth pointing out that in practice nobody knows how well things will actually bear out when these systems are in widespread deployment.

One problem is that rollups today are largely focused on reducing the computational burden of verifying transactions. This is a big deal, particularly for Ethereum where verifying complex smart contract executions is quite costly. But even with today’s rollups, L1 nodes are still expected to store and transmit the raw transaction data: without keeping these transactions around, the loss of a rollup server could freeze an entire smart contract in place, blocking any further progress. This means scaling bottlenecks still exist — they’ll just be hit when nodes run low on bandwidth and storage, rather than compute.

That’s still a potentially huge improvement and many folks are optimistic: Vitalik Buterin calculates maximum possible scaling improvements on the order of 100x for rollup servers, though he quickly tempers this calculation by noting practical concerns.

In any case, the point of this section is not to claim that scaling is a solved problem. Rather, the point here is that scale improvements are on the minds of a lot of smart engineers, and there are solutions on the way. The results might not be perfect and presumably there will be much experimentation before we settle on a workable approach, but the end result will almost certainly work fine at some level of scalability. The main question is simply how robust and decentralized the result will be.

Objection: “There is no privacy on blockchains (or there is too much privacy)”

Public blockchains rely on volunteers to operate a network that verifies transactions. The implication of this design is that the transaction data itself must be publicly viewable. While a few naive people still believe that these currencies anonymous, the truth is quite different: these older public chains expose your transactions to anyone who wants to see them. In those systems, your main protection is that transactions use a pseudonym (called an address) in place of your real identity.

Some advocates once felt that pseudonymity was good enough for privacy, but this belief has receded a bit as sophisticated “chain analysis” companies have grown up and made progress towards identifying the real owners of various accounts. The lack of privacy on these systems poses a real challenge for those who would like to build financial infrastructure on public chains.

The good news is that researchers have made a lot of progress on solving privacy problems around cryptocurrency. We now have deployed privacy tech that allows users to conduct transactions on public blockchains without revealing any information that they do not wish to reveal. These systems work by (effectively) encrypting transactions and using sophisticated zero-knowledge proofs to convince verifiers that the transactions data is consistent (i.e., that encrypted transaction amounts “add up” and do not create money out of thin air.) There now exist several deployed cryptocurrencies that provide strong privacy even against government surveillance, and law enforcement has expressed concerns about them.

Still, to criticize an early technology for being both private and not-private-enough has a “nobody goes there, it’s too crowded” feel to it. What is true is that over many years the traditional financial system has learned to walk a tightrope where customer privacy is balanced on one hand against anti-money-laundering regulations on the other (as regulated by laws like the Bank Secrecy Act in the US.) Achieving those goals in today’s financial infrastructure has not been without cost, however. Our privacy as individuals has been vastly degraded by technological developments, with little opportunity for democratic debate. And the result sucks: collecting all of our private data and securing it is expensive, an expense we all pay for in high fees and catastrophic breaches. The cryptographic privacy offered by cryptocurrency is exciting because offers a different road forward: one that promises to keep irrelevant data in our own hands.

The actual form that these mature systems take is unknown to me. Perhaps they’ll use zero-knowledge policies that keep smaller transactions private, while ensuring that larger transactions are known to regulators or other parties. I’m not excited to use those systems, because I think they’ll be risky. But at very least they’ll be better than our current collect-it-all-and-then-hand-it-to-hackers approach, which certainly has not done us very many favors.

So why do I care about any of this?

To put it simply: because payments are important. And because something is badly wrong.

Over the past four decades, computer networking has radically changed the economics of just about every industry that relies heavily on IT. Google made information access so easy that we can barely remember the world before it existed. My kids refuse to believe that I once paid $1/minute for long distance phone calls. It’s so inexpensive to start an online retailer that we now have more online pet food stores than we have drive-in movie theaters in the United States.

And yet if you looked at the money-transfer and payments industry, you’d see no such changes. Credit card merchant fees are similar, or have actually risen in the United States since the 1990s, and that is an absolute tragedy — since these fees are baked into the cost of most retail goods and thus fall heavily on the working poor (who pay them even if they use cash.)

If all you care about is technology, consumer payment tech has improved at a glacial pace. It took nearly two decades to roll out anti-fraud improvements like EMV chipchards and tap-to-pay (NFC) in the US. Shopping online in 1995 meant typing credit card numbers into webforms. In 2022… it mostly means exactly the same thing. As a result, online payment fraud has ballooned to around $200bn in 2020. And forget about real innovation like payment privacy or pay-by-phone (which is ubiquitous in Kenya and China but still in its infancy here in the US, and will likely only be “solved” by giving Apple and Google total control over payments.)

Why are these IT-focused industries so consistently immune to the same technological improvements and cost reductions we see everywhere else?

I’m only a computer scientist, so I’m going to let someone else answer that question. I can only tell you that what we have right now is not functioning properly: I suspect that legacy industry and regulators have smothered two generations of technological improvement, largely (I suspect) by building a (mostly) closed and permissioned financial system. And this is a big deal: payments are too important to our economy to entrust them to 1970s-era technology and an extractive industry. We don’t even know what novel applications — Googles, Facebooks, Wikipedias, Instagrams — we’re missing out on because the industry simply won’t allow them to exist.

I don’t know if blockchains are the solution to this problem. I see indications that the technology is finally starting to grow up in ways that seem like a harbinger of major positive changes on the horizon. Progress here is slow, though in some cases because the regulatory apparatus is throwing sand in the gears of cooperative products, and/or utterly failing to move expeditiously to uncover possible fraud. And maybe the result won’t even be a success for blockchain solutions: perhaps we’ll simply get more and better offerings from “traditional finance” industry as they start to wake up to the fact that more open systems can compete with their closed offerings.

So while I don’t know if cryptocurrency will be the answer, I’m just hopeful that something will be.

Title image by Flickr user Joegoauk Goa, used under CC license.